The enrollments apparently are now a trickle. The launch of the exchanges is now recognized as a "soft" launch. As expected, the state managed exchanges are performing marginally better than the federally run exchange

Exchange data. None of this is really surprising with the exception of the California data. They spent about $1 billion of Federal grant money to set up their exchange and they have enrolled no one? The Feds did not get their specs to the programmers until late this spring and there was no way this was going to get launched without serious bugs by the October 1 deadline. Given the other delays, the politics of this program where going to drive a launch by the October 1 deadline, come hell or high water.

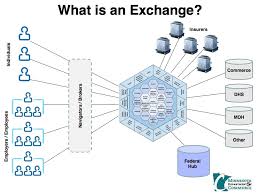

My state elected to allow the Feds to run their exchange. Now that people have been able to get access to the sites and see t he offerings, we are now getting a feel for what the insurance offerings and the networks look like. Similar to what has been observed in other states, the exchange here has offerings from a variety of insurers offering what appears to be much thinner networks than their usual products. For example, a number of the major health systems are not part of the Blue Cross and Blue Shield exchange offering. One thing I also did not realize is that those purchasing insurance through the exchange will get a tax break while those buying products outside of the exchange will not.

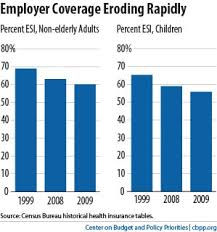

While the initial numbers insured through the exchanges may be small, over time they will grow for a number of reasons. First, the tax breaks available. This amounts to a subsidy independent of the direct subsidy. Second, there is going to be a transfer of those covered by employer based insurance to the exchanges. Employers will be able to better define and control their costs. They will simply say here is your money for insurance. Buy what suits your needs. While their will be push back to start, employees will adjust quickly. I can't say that I view this as a bad thing. Employer based health insurance created more problems than it solved.

There are going to be a lot of people who will be insured but because of the narrow networks the meaning of being insured will be very different. What happens when those who are insured have some sort of condition where the expertise to treat falls outside of the narrow network? What sort of language is within the contracts to address this situation? What will be the responsibilities of the physicians within the network? What will happen when patients are told that no one in your network knows how to help you?

I am sure that this will evolve over time and hopefully the most robust delivery systems will be able to put in place systems which can identify where expertise and capacity are needed. However, perhaps not. One business model may highlight strategic incompetence with very low rates to attract the well and frugal. I could imagine being able to deploy a network at very low cost if a system did not have to deal with any actual illness.

I look at our own practice which is the destination for a number of patients within a six state region. What happens when these patients start to come to us out of network and are expected to pay the entire cost of their care? While ostensibly insured, they are basically uninsured to us. What will be our ethical obligation to them? The simplest answers to this question will be either, we are physicians are we should care for them without concern for cost or we should treat only who can pay. Take the former tack and we will go broke an be of no use to anyone. Take the latter tack and we will have lost our way in terms of our mission. In addition, if patients have to pay full freight, our referral pipeline will likely dry up.

Sick patients will need to end up somewhere and if networks become increasingly closed and their ability to shunt patients elsewhere for specialist care is impaired, how will this play out? Remember this is all going to happen in a world where patients have increasing access to information. Patients will be able to change networks but movement of patients with serious illness from systems unable to care for them to networks able to take on challenges will need to be associated with the right actuarial data which will allow networks attracting the sick to remain financially viable. Being a magnet for patients expensive to care for is not a strategy for financial success if one cannot collect the premiums to cover your costs plus a reason rate of return.

There are going to be some gaping holes and some scary patient stories. However, there are gaping holes and scary patient stories now. It will be difficult to see if the holes will be bigger and the stories worse for a while. As they say, this is the fog of war....

No comments:

Post a Comment