However, creating rules and standard practices need to be viewed simply as starting points, not actual goals. The experience of the financial system over the past decade represents a cautionary tale and this is described in a WSJ piece "How regulators herded banks into trouble", written by Peter Wallison and published in this morning's paper.

http://online.wsj.com/article/SB10001424052970203833104577069911633739768.html?mod=WSJ_Opinion_LEFTTopOpinion&_nocache=1322941623984&user=welcome&mg=id-wsj

First, what is viewed as being safe bets at one point in time turn out to be risky and tragically bad bets at a different point in time. At the time the Basel Accords were adopted in 1988, mortgage based securities were viewed as the lowest risk investments banks could hold. The rules put in place at the time strongly encouraged commercial banks to hold these securities through capital rules, specifically allowing much greater leveraging when holding these debts (>50 fold) than with corporate loans (<20 fold).

The consequences of this huge miscalculation are described by Wallison:

Although these rules are intended to match capital requirements with the risk associated with each of these asset types, the match is very rough. Thus, financial institutions subject to the rules had substantially lower capital requirements for holding mortgage-backed securities than for holding corporate debt, even though we now know that the risks of MBS were greater, in some cases, than loans to companies. In other words, the U.S. financial crisis was made substantially worse because banks and other financial institutions were encouraged by the Basel rules to hold the very assets—mortgage-backed securities—that collapsed in value when the U.S. housing bubble deflated in 2007.

Today's European crisis illustrates the problem even more dramatically. Under the Basel rules, sovereign debt—even the debt of countries with weak economies such as Greece and Italy—is accorded a zero risk-weight. Holding sovereign debt provides banks with interest-earning investments that do not require them to raise any additional capital.

Accordingly, when banks in Europe and elsewhere were pressured by supervisors to raise their capital positions, many chose to sell other assets and increase their commitments to sovereign debt, especially the debt of weak governments offering high yields. If one of those countries should now default, a common shock like what happened in the U.S. in 2008 could well follow. But this time the European banks will be the ones most affected.Rules were created which were thought to match capital requirements with risk. They did not and because they were so successful in standardizing behavior before the rules were validated, they ended up magnifying the very events which they were deployed to prevent. Compliance with rules substituted for actually thinking about actual risk.

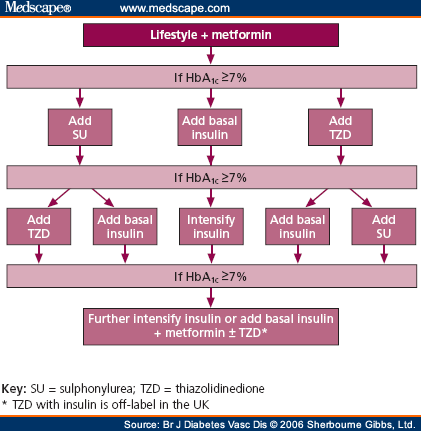

Throughout much of medicine there is a healthy push for standardization of practice and development of tools to assess aggregate success or failure. The problem we face is in the absence of a known superior standard, what standard practices do we push for before we have determined the best ones available? For the financial industry, they had a similar situation which resulted in both good news and bad news. The good news is they did figure out how to get banks to comply with a standard set of rules. The bad news is they were the wrong rules.

No comments:

Post a Comment